May 25, 2026

Electricity is becoming a strategic cost position – and most companies are not ready

ca.

4

Minuten Lesezeit

The energy transition is a power transition – with consequences for every energy-intensive budget

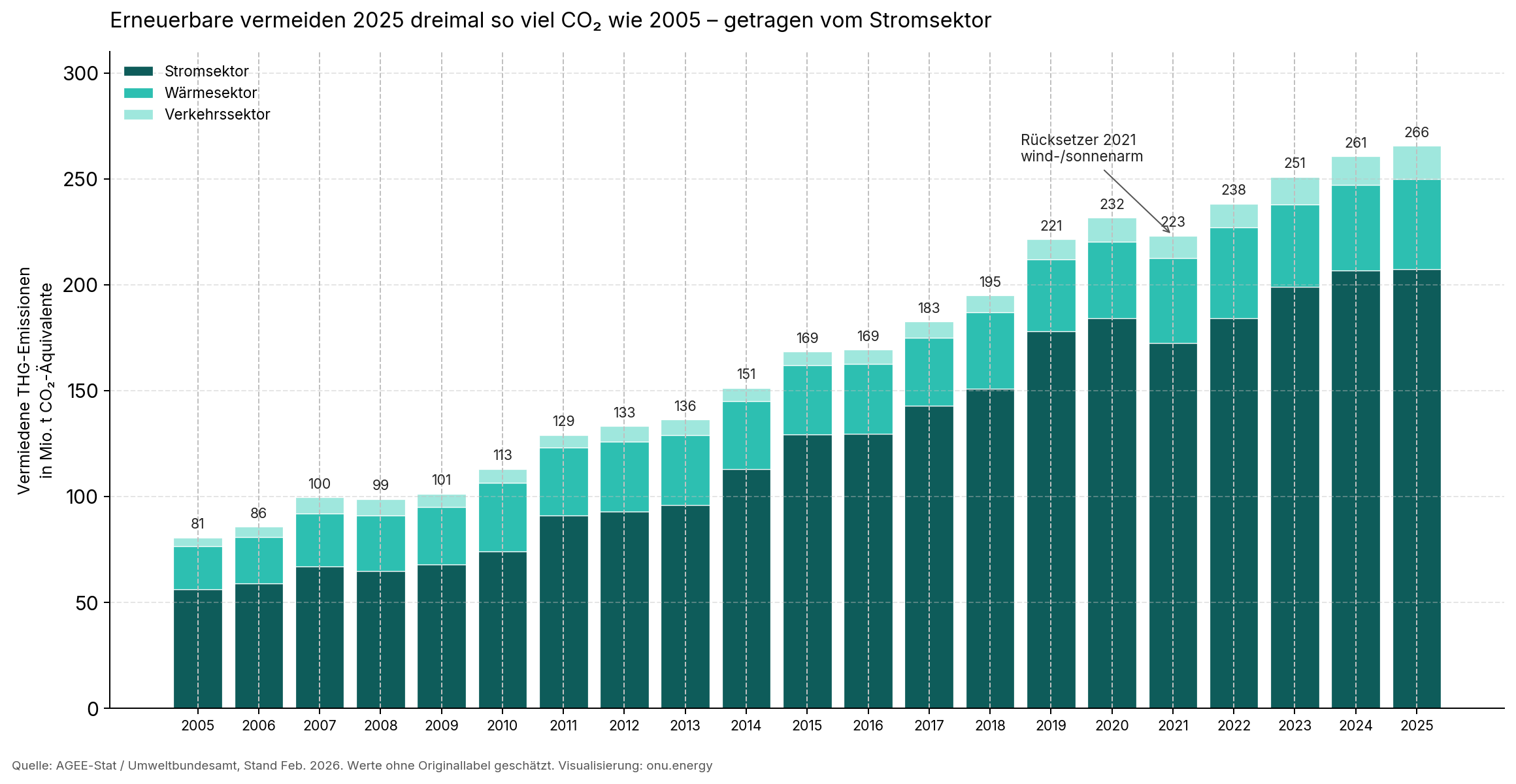

Renewable energy in Germany now avoids three times as many greenhouse gas emissions as in 2005 – from 81 to 265 million tonnes of CO₂ equivalent in 2025. That is an impressive figure. But it tells only half the story.

Look more closely and the picture sharpens: 78 % of this abatement comes from the power sector. Heat and transport are structurally lagging behind. Whether we like it or not, the energy transition is first and foremost an electricity transition. That has far-reaching consequences – not only for the climate balance sheet, but for the cost structure of every energy-intensive company.

The power sector is carrying the transition – and that comes at a price

The dominance of electricity in greenhouse gas abatement is no accident. Wind and solar are scalable, can be deployed quickly, and are now among the cheapest forms of generation. At the same time, industry is electrifying processes that used to run on gas or oil: heat pumps, electrolysers, induction furnaces, compressed air, cooling.

The result: for producers – from dairies to metal processors – electricity is becoming the dominant energy cost line. What used to be one item among many is turning into a strategic variable that shapes margins, competitiveness, and investment decisions.

For food producers with constant baseloads for cooling, processing, and storage, that is already reality today. For chemicals, paper, glass, and metals it will become even more pronounced in the years ahead. Anyone who does not treat renewable generation and consumption as a system underestimates the shift – as we set out in Why solar alone is not enough.

What the data also show: volatility is the system, not the exception

2021 stands out in the statistics: avoided emissions fell from 232 to 223 million tonnes – a setback of almost 9 million tonnes because the year was low on wind and sun. Fossil plants stepped in, and power prices rose.

For companies this means: an energy system that relies on weather-dependent sources for 78 % of its abatement is structurally volatile. Price swings of 30, 50, or 100 % within a year are no longer exceptions – they are the new normal. Anyone who does not actively manage electricity procurement leaves a growing share of the cost base to chance. Flexibility, storage, and controllable load become strategic levers – topics we explore in the context of BESS in industrial use and the regulatory outlook for renewables (renewables expansion moratorium and transition reality).

The strategic question for CFOs: how well are we positioned?

Many companies have historically treated energy procurement as an operational process – annual tender, framework contract, done. That logic works in a stable, fossil-dominated market. It no longer works in a market shaped by renewables, intraday volatility, and policy intervention – a pattern we described for mid-sized industry in why energy procurement in the Mittelstand must work differently today.

The questions boards and CFOs need to answer today:

How large is our electricity cost share today – and where will it be in five years?

Anyone planning electrification pathways must model power as a growing budget line, not a fixed cost.

Do we have a hedging strategy – or are we buying reactively?

Spot exposure in a volatile market is an implicit bet. If you do not take it consciously, you still take it.

Are we using the opportunities the market offers?

Renewables regularly produce surplus power at negative or very low prices. Companies that are flexible enough can benefit – through controllable load, storage, or intelligent procurement strategies, as outlined in cutting energy costs through smarter procurement.

Can we explain our energy strategy to investors, customers, and regulators?

CSRD, Scope 2 reporting, and supply-chain requirements are turning energy procurement into a governance issue.

Think strategically before the market forces you to

Companies that invest in strategic energy procurement today secure a structural cost advantage over competitors that keep buying reactively. That applies to a dairy with three sites as much as to a automotive supplier with twelve plants in four countries.

The energy transition is not an external threat to react to. It is a market shift you can capitalise on – if you build the right structures early: data-driven load forecasting, active hedging, use of PPAs, and a clear view of your procurement position versus peers. Examples of how that pays off in multi-site control are discussed in the Flender case study on steerable energy procurement.

Electricity was long taken for granted. It is becoming a core competence. onu.energy helps large industrial consumers align power costs, hedging, and procurement strategy in one steering view – before the market makes the decision for them.

Data source: AGEE-Stat using data from the German Environment Agency (Umweltbundesamt), as of February 2026.